Welcome to our insightful blog that delves into the vital topic of “Eligibility to Claim Input Tax Credit under GST.” In the landscape of taxation, understanding input tax credit (ITC) eligibility is paramount for businesses seeking to optimize their financial operations. This comprehensive guide will unravel the nuances of ITC, shedding light on the criteria that determine a business’s entitlement to claim this credit. Join us as we explore the crucial factors, compliance requirements, and strategic considerations that empower businesses to navigate the realm of input tax credit with confidence and precision.

|

Table of Contents |

Meaning of Input tax credit

In the context of the Goods and Services Tax (GST), Input Tax Credit (ITC) is a mechanism that enables businesses to offset the tax they have paid on inputs (raw materials, goods, or services) against the tax they are required to pay on output supplies. In other terms, it allows a business to deduct the tax already paid on purchases from the tax owed on sales.

Input tax credit is designed to eradicate the cascading effect of taxes, in which taxes are levied on taxes, resulting in increased costs for businesses and final consumers. With ITC, the tax is calculated based solely on the value added at each stage of the supply chain, resulting in a more efficient and transparent system.

For instance, if a manufacturer purchases raw materials and pays GST on those materials, they can deduct this amount from the GST they collect from customers when selling finished products. This ensures that only the value added at each stage is taxed, as opposed to the entire value being taxed multiple times.

Who can file for ITC?

ITC can only be claimed by a GST-registered individual who meets ALL the prescribed conditions.

- The dealer must possess the tax invoice.

- The dealer must have received the goods or services.

- Returns must have been submitted.

- The supplier has already paid the levy to the government.

- When products are received in instalments, ITC can only be claimed upon receipt of the final shipment.

- No ITC will be granted if depreciation has been claimed on a capital asset’s tax component.

- A taxpayer enrolled under the GST composition scheme cannot claim ITC.

Conditions for ITC Claiming

The eligibility to submit an ITC claim is contingent upon both “conditions precedent” and “conditions subsequent.” This entails two points. Certain conditions must be met prior to and some after claiming the credit to maintain compliance with the GST regime.

Prerequisite conditions for claiming ITC

The registered person may claim a credit for the acquisition of inputs, input services, or capital goods used in the conduct of business or for business purposes. It should be noted that an entity with an active GST registration will be able to claim input tax credits for purchases made for business purposes. Once this primary condition is met, taxpayers must ensure that the subsequent conditions are met in full to exercise the vested right.

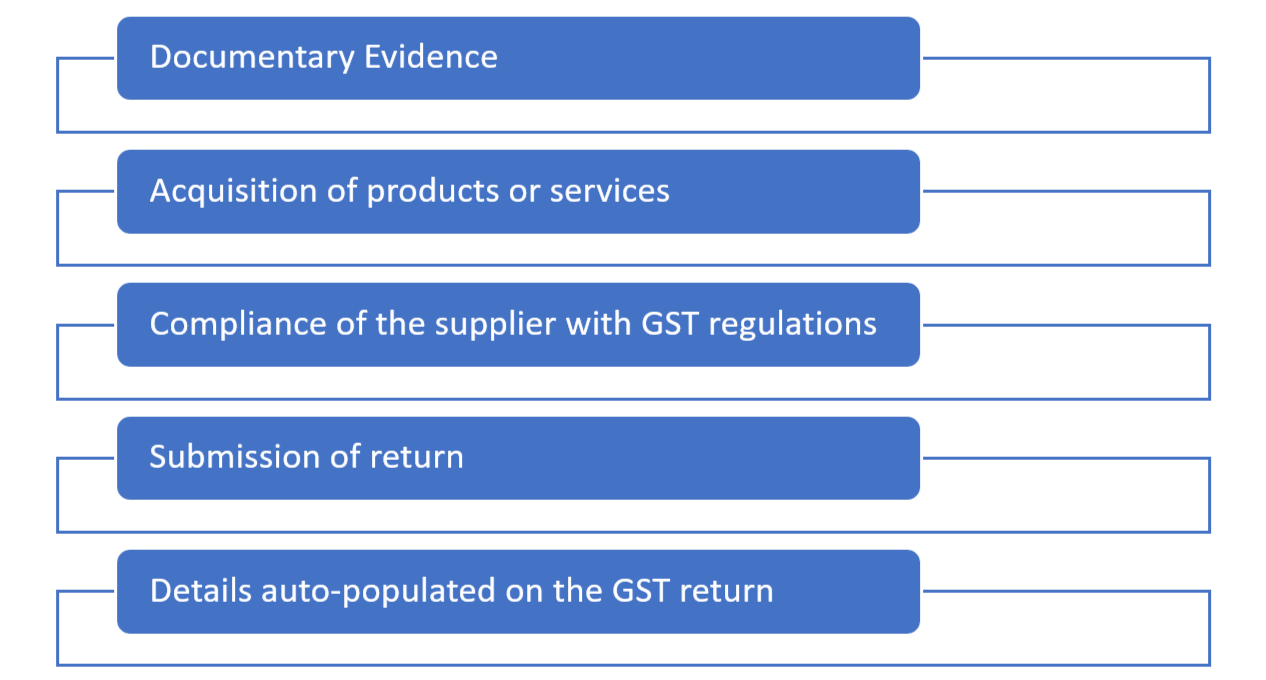

- Documentary evidence: It is the initial requirement for claiming ITC, and includes tax invoices, debit notes, and bills of entry. One must ensure that the tax invoice complies with the applicable e-invoicing requirements.

If the supplier fails to comply with these provisions, the ITC may prohibit the recipient (or purchaser). A self-invoice would suffice as a valid document for availing credit when the supply is subject to reverse charge (i.e., the recipient is responsible for paying the tax).

- Acquisition of products or services: The products or services must have been delivered to the recipient. In cases where the invoice pertains to the previous month, but the actual receipt occurs in the following month, the ITC on such supplies is deferred until the following month. Notably, if the supply is received by another person on the recipient’s instruction, the supply will be deemed to have been received by the recipient. This is commonly referred to as the “bill to ship to” scenario.

- Compliance of the supplier with GST regulations: Importantly, the purchaser must deposit the tax collected from the recipient into the government’s account. This condition imposes on the recipient the onerous duty of ensuring that the supplier deposits the collected tax into the government’s treasury. Notably, the recipient is not provided with a mechanism to assure such fulfilment, resulting in a situation where the recipient’s legitimate credit is contingent on the supplier’s tax payment.

- Details auto-populated on the GST return: ITC eligibility is restricted to the information provided by the supplier on Form GSTR-1 as part of their monthly GST compliance obligations. Thus, beneficiaries can only claim credit for invoices reflected in their Form GSTR-2A/2B for the relevant month. This requirement requires taxpayers to perform reconciliation on a regular basis to ensure that the invoices in their records correspond to the supplier’s filings.

- Submission of return: The recipient must submit GST returns to claim input tax credits. Consequently, it is essential to ensure that the conditions are met for the recipient to claim input tax credit.

Post conditions of ITC eligibility

Taxpayers should consider the following parameters to ensure that the ITC claimed is utilized properly.

- Payment to the vendor within 180 days: To avoid incurring interest charges, taxpayers must pay their vendors within 180 days of the invoice date. Failure to pay within the specified period results in the reversal of ITC and interest liability. This condition does not, however, apply to reverse charge transactions, the importation of products, or transactions between related and unrelated parties.

- ITC is neither restricted nor ineligible: Taxpayers should ensure that their ITC claims do not fall under the GST’s ‘blocked credit’ category. Particularly when rate notifications restrict ITC claims, extreme caution is required.

- The deadline for claiming input tax credit: ITC for a financial year must be claimed until 30 November of the following year or the due date of the annual return, whichever is earlier. Even if all the requirements are met, any unclaimed ITC after the deadline will expire and become inaccessible. Therefore, the timely availability of ITC under GST is essential for maximizing its benefits and avoiding the loss of eligible credits.

If the ITC claimed exceeds the GST output tax liability, taxpayers may carry such accumulated ITC forward indefinitely to subsequent fiscal years. In the case of export-rated supplies of products or services, the accumulated ITC can be refunded to the taxpayer. Similarly, in certain domestic transactions, taxpayers can request a refund of the accumulated ITC. This includes instances in which the credit has accumulated because of an inverted duty structure, in which the tax paid on input supplies is greater than the tax payable on output supplies. However, it is essential to observe that the ITC refund on capital goods is limited.

Conclusion

In conclusion, grasping the eligibility criteria for claiming input tax credit under GST is pivotal for businesses striving for financial efficiency. By ensuring adherence to these criteria, businesses can unlock opportunities to offset their tax liabilities and enhance their bottom line. Remember, maintaining accurate records, complying with GST regulations, and staying updated with evolving guidelines are key to maximizing input tax credit benefits. As the GST landscape evolves, an initiative-taking approach to understanding eligibility will not only streamline financial operations but also contribute to the growth and compliance of your business.