| Table of Content |

What does set-off of loss means?

Set off of losses means adjusting the losses of current year or previous year against the profit or income of the current year. If loss of the one year is not set off against the income of the same year than that loss can be carried forward to the subsequent years for set off against income of those years.

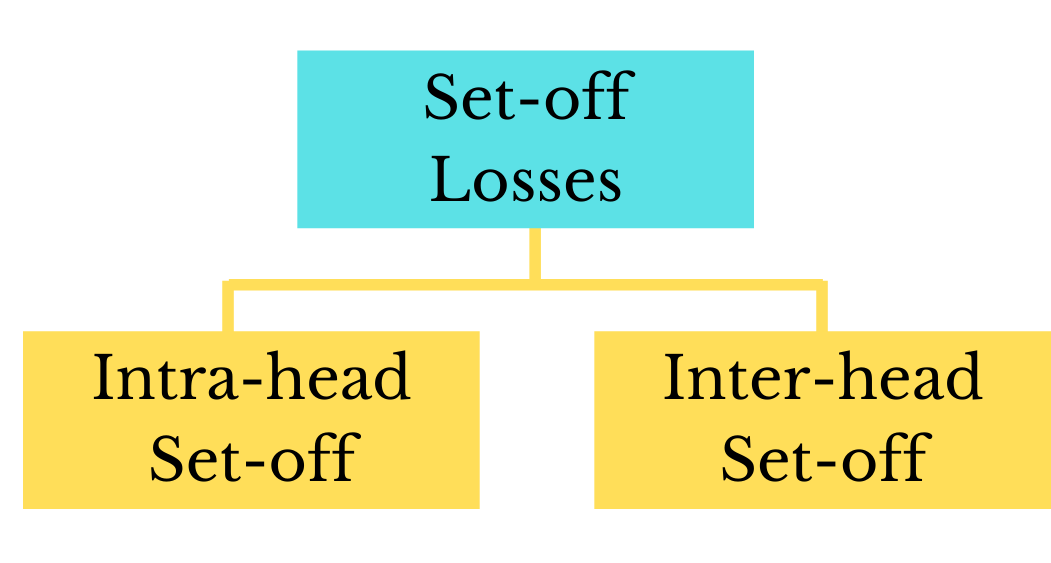

Set-off losses can be of two types:

Intra-head Set Off

Intra head set-off means the losses of the one source of income will be set off against income from another source under the same head of income.

Example: Loss of Business A can be set off against profit of Business B, where Business A is one source and Business B is another source and the common head of income is “income from business and profession”.

Exception of Intra-head set-off

- Long term capital loss

- Loss from speculative business

- Loss from owing and maintaining race horse

- Loss from business specified under section 35AD will be set-off against specified business

Inter-head Set-Off

Inter head set-off means loss under one head will be allowed to set-off against the income for that assessment year under any other head.

Exception of Inter-head set-off

- Losses under head Income from business or profession will not be set-off against salary income

- Loss of business specified under section 35AD can be set off only against specified business

- Losses under Capital gain cannot set-off against any other head income

- Loss from activity of owning and maintaining of horses cannot be set-off against any other type of income.

- Loss under head income from house property can be set-off against any other head income only to the extent of 2lakhs. That means maximum loss from house property which can be set-off against the income of any other head is 2lakh.

For better understanding we have summed up the tabular summary for adjustment of losses where yes denotes that the losses can be adjusted and no denotes the opposite

| Incomes | Long term capital loss | Short term capital loss | Loss from owning and maintenance of race horses | Loss under the head House Property | Speculative business loss | Other business or professional loss |

| Salary | No | No | No | Yes | No | No |

| House Property | No | No | No | Yes | No | Yes |

| Non Speculative Business | No | No | No | Yes | No | Yes |

| Speculative Business | No | Yes | No | Yes | Yes | Yes |

| LTCG | Yes | Yes | No | Yes | No | Yes |

| STCG | No | No | No | Yes | No | Yes |

| Owning & maintenance of race horses | No | No | Yes | Yes | No | Yes |

| Others | No | No | No | Yes | No | Yes |

Carry forward losses and set-off

House Property (Section 71B)

- Losses of house property can be set-off in the same assessment year from the income of any other head

- Loss of house property can be carry forward up to next 8 assessment years from the assessment year in which the loss was incurred. And will be adjusted only against Income from house property

- Losses of house property can be carried forward even if the return of income for the loss year is belatedly filed.

Business losses (Section 72)

- Loss of “Profit and gain from business or profession” PGBP other than loss from speculation business can be set off against any other heads income in the same assessment year

- And if such loss cannot be set-off against income from any other head the loss shall be carried forward to the following assessment years and it shall settled against the income from business and profession

- The loss from business and profession can be carried and set off against the profit of the assesse who incurred the loss. That means the person who has incurred the loss will entitled to carry forward the loss and set-off the same

- Loss of business or profession can be carry forward up to next 8 assessment years from the assessment year in which the loss was incurred. And will be adjusted only against profit and gains from business and profession

- As per section 80, the assesse must have filled a return of loss u/s 139(3) in order to carry forward and set off a loss

Loss in speculation business (Section 73)

- The loss from speculation business can be set-off only against the income of speculation business

- The loss if not fully set-off against the income of speculation business can be carry forward up to the next 4 assessment year from the year of loss.

Speculation transaction means a transaction which:

- Contract of purchase and sale of commodity including stock and shares other than actual delivery r transfer of commodity or stock

Losses of business specified u/s 35AD (Section 73A)

- Loss of any business specified u/s 35AD shall be allowed to be set-off against the income of any other specified business under PGBP

- If loss of the assessment year is not set-off fully against the profit of the assessment year shall be allowed to carry forward the loss up to the “n” numbers of year (without limit) and can be set-off against the income from the specified business u/s 35AD.

- This means the loss of specified business cannot be set off against the income of any other non-specified business not in current year.

- The losses can be carried forward in the following year even if the assesse has not filed the return of losses (section 80)

Losses under Capital gain (Section 74)

- Loss of Capital gain will be set-off against the income of the same head under in respect of any other capital gain income

- Long term capital gain will be set-off with only long term capital gain and not from other

- Short term capital gain can be set-off from both shot as well as long term capital gain

- If loss of capital gain is not set-off from the profit of current year can be carried forward the loss to the following year up to 8 years from assessment year loss is computed.

Loss of other source (Section 74A)

- The loss of owning and maintaining race horses shall be set-off only against the income of owing and maintain race horses in that year and shall be carried forward to the following assessment years

- It shall be set off against the income from the activity of owing and maintaining race horse assessable for the A/Y provided that the activity of owning and maintain race horse is carried on be him in the P/Y relevant for that A/Y

- If losses are not set-off fully in the current year can be carried forward up to 4 years from the assessment year of loss.

| S.no. | Nature of loss to be carried forward | Maximum permissible period [from the end of the relevant assessment year] for carry forward of losses |

| 1 | Unabsorbed loss from house property | 8 assessment years |

| 2 | Unabsorbed business loss (non- speculative) | 8 assessment years |

| 3 | Loss from speculation business | 4 assessment years |

| 4 | Loss from specified business under section 35AD | Indefinite period |

| 5 | Long-term capital loss | 8 assessment years |

| 6 | Short-term capital loss | 8 assessment years |

| 7 | Loss from the activity of owning and maintaining race horses | 4 assessment years |

Order of set-off of losses

As per section 72(2), brought forward business loss is to be set-off before setting off unabsorbed depreciation. Therefore, the order in which carry forward and set-off is as follows:

{kind=link}