The spread of Novel Corona Virus (COVID-19) across many countries of the world, including India, has caused immense loss to the lives of people and resultantly impacted the trade and industry. In view of the emergent situation and challenges faced by taxpayers in meeting the compliance requirements under various provisions of the Central Goods and Services Tax Act, 2017 (hereinafter referred to as the “CGST Act”), Government has announced various relief measures relating to statutory and regulatory compliance matters across sectors.

- Section 10 of CGST 2017 Act deals with the Provisions related to composition levy. Central government by its official notice announced that registered person who opts to pay tax under section 10 of CGST Act 2017 for the financial year 2020-21 shall electronically file intimation in FORM GST CMP-02, duly signed or verified through electronic verification code, on the common portal, on or before 30th day of June, 2020. And shall furnish the statement in FORM GST ITC-03 in accordance with the provisions of sub-rule (4) of rule 44 up to 31st July, 2020.

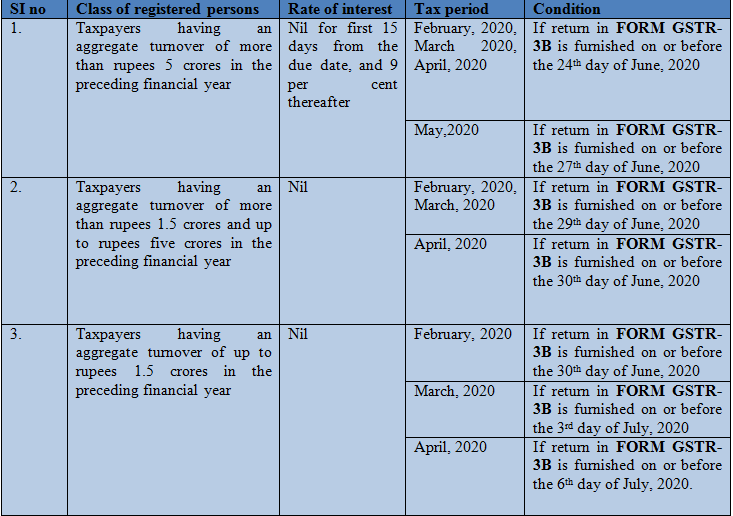

- Relaxation given to the registered person who are required to furnish the returns in FORM GSTR-3B, but fail to furnish the same along with payment of tax for the months given below in the table can furnish the said return according to the condition mentioned in the corresponding Table, namely:

- If a registered person who fail to furnish the details of outward supplies for the said periods in FORM GSTR-1 by the due date, but furnishes the said details in FORM GSTR-1, on or before the 30th day of June, 2020.Late fee payable under section 47 of the CGST Act shall be stand waived for the months of March, 2020, April, 2020 and May, 2020, and for the quarter Jan to March, 2020.

- Registered persons registered under composition scheme shall furnish a statement, containing the details of payment of self-assessed tax in FORM GST CMP-08 of the Central Goods and Services Tax Rules, 2017, for the quarter ending 31st March, 2020, till the 7th July, 2020.

- Registered person shall furnish the return in FORM GSTR-4 of the Central Goods and Services Tax Rules, 2017, for the financial year ending 31st March, 2020, till the 15th day of July, 2020.

- No need for re-opting for the composition scheme: The taxpayers who are already in composition scheme, in previous financial year are not required to opt in for composition again for FY 2020-2021.

- Normal Taxpayers wanting to opt for Composition should not file GSTR3B and GSTR 1 for any tax period of FY 2020-21 from any of the GSTIN on the associated PAN.

- Where an E-way bill has been generated under rule 138 of the Central Goods and Services Tax Rules, 2017 and its period of validity expires during the period 20th day of March, 2020 to 15th day of April, 2020, the validity period of such e-way bill shall be deemed to have been extended till the 30th day of April, 2020.

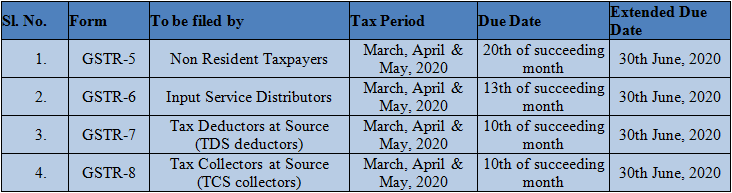

- For Non Residence Taxable Person, Input Service Distributer, Tax Deductor at Source & Tax Collector at Source taxpayers:

This notification shall come into force with effect from the 20th day of March, 2020.

{kind=link}